I have briefly mentioned in previous updates that one of my brothers is a portfolio manager with a significant institutional investment shop. He is the first person I reach out to when the three of us here become overly perplexed, excited, or frustrated by something we are pondering within financial markets. He often does the same on his end. On one hand, we operate in the same world in that our jobs are almost entirely focused and dependent on financial markets over which we have no control - problematic for two admitted control freaks as you might imagine. On the other, our worlds couldn’t be any more different. He is mandated to invest only in stocks for his clients, while I have the vast majority of asset classes at my disposal. As such, he doesn’t have to concern himself with market risk, the macro environment, or anything to do with his clients’ long-term financial plans – he is only concerned with his portfolio beating a pre-determined benchmark. I, on the other hand, am almost exclusively concerned with the former on clients’ behalf – and as such – spend next to zero time fretting over whether stock “x” will outperform stock “y” in the next quarter (we hire people like him to make those decisions). Most of our conversations around the world of finance end with him telling me that, “You couldn’t pay me enough to have to make the decisions you do in this environment”, and/or me saying the same to him – albeit for totally different reasons. Though I will say there are times where we are telling each other the opposite – that “I’d give anything to trade with you right now” (this year was my turn). There is a point to this, I promise…

While our jobs are similar, and we come from the same gene pool, the way we analyze things often couldn’t be more different. We are both overly analytical, and extremely forward looking. The seemingly generational shift that has occurred from long-term thinking to short apparently escaped us. Yet the manner in which we analyze information is what is so different. He may disagree, but I would say neither of us possess more “book smarts” than the other – though I will point out (since he is reading this) that I have a full 2 more post-graduate degrees than he does. Take that! Similarly, we’ve both been in this investment world for what feels like forever – acquiring what I would call “street smarts” for the sake of this discussion. While we each rely on both, the main difference between our analytical styles stems more from how we weigh the two – he might lean more heavily on the former while I am less inclined to ignore the latter.

Might not sound like much of a difference, but we fight like cats and dogs on a lot of things – though interestingly, rarely about financial markets. For better or worse, we are pretty well aligned in our views about the current state of the financial system at large – taking a long-term view. But we discuss just about everything – from sports to politics to society and everything in between. And there is one statement that – when I throw it out there in our conversations – simply infuriates him. The conversation turns into a shouting match instantly upon my using it. Based on the description above, one will understand why. The statement, you ask?

“It’s common sense.”

Now first off, let me be the first to admit my understanding as to why that statement can be infuriating to some. Simply put, what is “common sense” to me might certainly not be to you. The two words together automatically imply “opinion” over “fact”. At the same time, if I could get feedback from every single person reading this right now to the question, “Could the world use a little more common sense at the moment?”, my guess is that the overwhelming answer would be “yes”. As with most things in life, I would surmise that the best analysis of anything comes from a healthy dose of both data and experience – “book” and “street” if you will – with the ever so important mandates of recognizing and removing one’s bias, and being willing to consider outcomes that don’t match your own conclusions.

Moving away from my brother – though I thank him for his unwitting participation in this update – and on to our outlook for the coming year. Few things. First, this is going to be much more straight forward and “less technical” than some of the other updates or outlooks that we produce. We covered a lot of the technical stuff in the update in July, and not much has changed (at least in terms of what was being analyzed) since. Next, we are skipping the always comical (at least to us) “predictions” for the coming year. The rest of this outlook will be our explanation as to why we made this decision, but simply put, we see 2024 as a straight coin-flip on just about every level. While we acknowledge as much about the outlook for any given 12-month period (which is why we laugh), we normally at least have strong opinions behind our guesses for the year ahead. If this was an outlook for 2024-2026, we could oblige with more confidence again this year, as our longer-term outlook on the economy remains largely unchanged for reasons we will again discuss. But 2024 is awfully tough to get a handle on, particularly with how 2023 played out, and in light of a particularly important factor we will share at the end. Again, this will make more sense as you continue reading…

We are also combining our “what we got right/wrong” and “summary of the past year” into this one paragraph. No, it is not because we got more wrong than we did right with our “predictions” for 2023 – though that would be an understatement at best. As we have mentioned before, all current and previous updates remain on the website – so they are all there in all of their glory if you would like to revisit on your own. The following will be our best attempt at summarizing this crazy year into a single paragraph:

A volatile year for both stocks and bonds, beginning with a continuation of what we then believed to be a run-of-the-mill, forward-looking, bear market rally. Cracks then began showing in the banking system, with a bank of significant size (and stature to some) failing. Stocks understandably reversed lower as depositors began withdrawing their monies from small and mid-sized banks out of some combination of fear, and the fact that they could get much better interest rates elsewhere. Somewhat surprisingly – yet at this point, shame on us for even saying so – the combination of Yellen and J-Pow came to the rescue. The former cryptically announced that “all bank deposits are safe” (what is the point of FDIC?), and the latter opened yet another Fed facility where banks which were struggling with government bonds on their balance sheets – which in some cases had lost more than half of their market value due to the now much higher interest rates (where were the regulators?) – could now “exchange” said bonds with the Fed (as some sort of loan) as a way of “recapitalizing” them (sound familiar?). Not (entirely) surprisingly, stocks reversed course higher in reaction to the latest Fed/Government intervention, until longer-term interest rates – which had by now reached their highest point in some 15 years – finally took the legs out of the market again in the fall. Stocks again managed to stem the downtrend in early November – helped along by Yellen deciding to monkey around with how they were funding the ever-growing debt, causing longer-term rates to ease significantly. At this point, we finally saw some names outside of the “Magnificent 7” begin participating. This was most interesting, as for much of the year only 7 stocks had accounted for most (or all) of the gains in the S&P 500 - though it also felt eerily similar to a short squeeze coming out of the downtrend in October. There were many – ourselves included – that thought the downtrend in October might have signalled the end of a “trap door” in a more prolonged bear cycle. Finally, only 3 days ago as of this writing, J Powell came out and not only held interest rates where they were (expected by most all), but then started adamantly and completely unexpectedly talking about the possibility of cutting interest rates early next year. This after only 30 days prior stating that, “We are not even talking about the possibility of rate cuts…”, and with no surprising data of note having been released between the 2 statements. At this point, prices of virtually all asset classes ripped higher in response, which is where we sit today.

OK, that was long, but not bad cramming all that we just experienced into just one paragraph! Onto how it all affected our (general) positioning. The “chop” (volatility) killed our trend-following position, which proved beyond frustrating as the position served as a primary source of “growth” exposure for us (in a market fueled by “growth” all year). But the most frustrating (and astounding at this point) aspect of this year – at least until the last 2 weeks – was the severity of the relative performance of “growth” over “value”. We have a heavy tilt toward the latter. As we have discussed before, the main justification for valuations on growth stocks over the 10 years of near-zero interest rates was that “growth stocks are duration assets”. Meaning that when interest rates are low (or certainly zero), one would pay more for the earnings growth associated with these stocks (i.e., “valuations don’t matter”). We might have disagreed with the simplicity of their analysis (we did/do), but at least to date, they have been right and we have been wrong. We can accept that. But to then tell us that with interest rates rising 5%+ at the fastest clip in our country’s history – with inflation to boot (arguably much better for many “value” stocks) – and the NASDAQ is going to rise near 50% this year while the rest of the stock universe will do little in comparison? We’ve either gotten to the point of absurdity, or there is something else going on – both are entirely plausible. This will be the basis for much of what follows below…

One of the few things we did get “right” this year was adding duration (interest rate sensitivity) when we did. As we mentioned last year, it was our positioning in the income space that has been the biggest (not only) driver of our relative (and dwindling) outperformance over the past 2 years vs. the “models”. How and when to begin adding back duration was on top of our list of discussions coming into the year, and luckily (it’s always luck in the short-term) – our timing of doing so worked very well. But as we have discussed with some of you lately, even that has been frustrating in the past few weeks as we don’t yet have the size of exposure that we would like – and longer-term interest rates have now followed stocks in their video-game-like moves - dropping over a full 1% in just over a month. That ain’t normal folks – and moves like that are usually associated with periods of extreme financial stress…or in third-world economies. To our knowledge, neither is currently the case here. Anyway, great for the positioning we added during the year – but we are already now left wondering just how much “meat is left on that bone (position)”, when only a month prior we viewed the space as the best long-term, risk-adjusted opportunity available. Fascinating times for sure….

With that, we take a look at our cards – knowing we must always play the hand we are dealt – and move on to 2024. A couple of quick and very important notes before we get into our outlook for the year ahead:

OPENING NOTE #1 – Jerome Powell Decision/Press Conference This Week

If you are the type that is interested in following this stuff, read on from here – if not, skip to note #2 below (the most important section of this update by far). My initial reaction to Powell’s words this week – believe it or not – was that he was making the right decision. This, of course, is assuming that he was acting/speaking based on the state of the economy. You know, like doing his job. As we will note, we are skeptical that the consumer can much longer handle the now much higher interest rates on top of the now much higher price of everything – in an economy fueled by debt – so signaling rate relief going forward would seem like a prudent and proactive move in our view.

But the more we analyzed it, it became more and more plausible that his rather shocking change of heart may have been more “political” than not. The “extreme” theory would be that either the administration strong-armed him into saying what he said, for their political gain going into the election – or that he chose this path on his own, given the rather polarizing figure that lurks on the other side. The “less extreme” version would be that by saying what he said now, he can now be “hawkish” next year (as deemed necessary) simply by not cutting rates – as he has now led markets to believe that he would in fact be doing so – rather than having to increase rates during an election year, and catching all the flack that comes with it. Both are plausible – but if he is in fact acting “politically” - we would view the latter as more likely.

Either way, we are not saying this for the purpose of political commentary – we are discussing it because it matters. One of the lessons we have certainly learned over the past 15 years is that the Fed can have a lot to do with asset prices. If the Fed is going to ease financial conditions solely because of an election – and ignore the actual state of the economy – then that would potentially be a very significant tailwind to asset prices in the short-term. It would also lend us to consider adding additional commodity exposure, because of the risks of inflation coming back. Finally, it might (interestingly) cause us to rethink how much exposure we would want to interest-rate sensitivity – as the bond market might decide to take actions into its own hands next year (longer-term rates rising) should it start worrying about inflation again.

Conversely, if we assume that he made this decision the way he is supposed to – based on his assessment of the economic conditions going forward – one might then wonder, “What do they know that they are not telling us?” When we say that it was a shocking change of tone, we are not saying that lightly. It was clear that he was not mincing any words. If we operate under this assumption, it might be Powell foreshadowing that the lag effects of raising interest rates – which we have discussed so many times in the past two years – are about to show themselves...and he knows it.

Overly simplified discussion – but important to note in an update about the coming year. If you are interested in more, I’d encourage you to listen to the last two press conferences he gave, and come to your own conclusions. We’d be interested in hearing your thoughts…

OPENING NOTE #2 – About Valuations

Everyone is required to read this section – and I am going to make it super simple. Some of you may be thinking to yourselves right now, “Oh God, not valuations again….” A few of you have even said as much about the topic in our recent conversations. First off, let me say this. If you are tired of hearing about valuations from us, can you imagine how exhausted we are in talking or writing about them? You have no idea. Still, let me share a fact. Note, I said “fact” – I did not call it an opinion:

Valuations. Matter. With. Investing.

If you believe otherwise, then you are in essence saying that you are much more interested in trading or “gambling”(speculating) – basically one in the same on most levels – rather than “investing”. Or, you believe that financial markets are now a “rigged game” – pretty much one in the same again. It is very true, valuations mean little for short-term trading – trend, technicals (and luck) matter much more. But if you deem yourself a long-term investor – which remains our assumption for any client reading this – then valuations have to matter. Let us explain…

A purely hypothetical example here. Let’s say that you could buy and own entirely a business for $100,000. Said business averaged $6,000 of annual profits over the past 10 years. We are going to ignore both the potential risks and potential growth for those earnings going forward in this example for simplicity. Assuming as much, your “earnings yield” – or expected annual return – by buying this business is 6% ($6,000 annual return divided by $100,000 investment).

Using today’s environment, let’s say you could instead take your $100,000 and invest it in US government bonds maturing in 10 years and at a 4% interest rate. Doing so generates $4,000 per year of income – no more, no less. Then, in ten years (assuming you hold it), you will get your full $100,000 back – no more, no less.

In weighing this investment decision – and yes, I fully understand that I am ignoring inflation and a million other risks with either – the business doesn’t sound like a bad bet. Reasonably sound 6% return, and it handily beats the $4,000 you would earn with the bonds. Make sense, right?

Let’s change it up a bit. What if I told you that the value of the fictional business above had risen to where you would now have to invest $300,000 to buy it – and the earnings would remain the same. Well, this changes everything. Your earnings yield based on this price now drops to 2% ($6,000 annual return divided by $300,000 investment). Not nearly as attractive – especially with interest rates on risk-free bonds significantly higher than the now 2% earnings yield on the business.

If you followed along with the example above, you now understand “valuations”, now and forever. Way, way, way over-simplified – but also plenty enough to work with. Using the hypothetical above, the “$100,000” represents your investment portfolio – every day, we are trying our best to make these decisions on your behalf. The business represents “stocks” – literally. Purchasing a stock (or a basket of stocks) is nothing more or less than purchasing a share of a business’ future earnings. They really aren’t random entities within some video game that show up on the news each night, and on your statements at the end of every month. Who knew?!

The “government bonds” represent, well, government bonds. That’s exactly what they are and how they work – with a whole lot of complexity surrounding duration that we will not get into here.

If we wanted to expand another 20 pages on this hypothetical (we don’t), we could make “value vs growth” – along with about 100 other financial metrics – make sense as well. All we really ask is that you understand what is above. Let’s add one final piece, to tie everything together…

Using the same hypothetical business, let’s say your best friend came to you and said, “Hey, I own a similar business and I could already sell it for 50% more than what I paid for it last year! You need to get in!” Uh oh, you just got nervous. You know your friend has been making a fortune (she tells you all the time), and you don’t want to make a mistake and miss out on these giant returns (FOMO). But you also know nothing about her financial situation, who is advising her, what might cause this to be true or not, etc. – and based on the math you did above – you know that if the business did go up another 50%, your “earnings yield” would now be less than 1.5%. Why would someone be willing to buy that from me at that point? Still, this just added a whole lot of anxiety to an already stressful decision.

Welcome to “speculation”, or what we lovingly refer to as “gambling”…and the world of “FOMO”

If you follow and understand everything we have shared above – even though it is overly simplified – then you will understand why we believe valuations matter….long-term. To reiterate, they matter little in the short-term…until they (historically) matter a lot. Using our example above, if we buy the business at $100,000 with a 6% income stream (and assuming the business is a solid one), there is only so far the value would assumptively fall before someone came in to snap it up. Conversely, if we paid $300,000 for it, during a period of speculation – but it ultimately returned to its “inherent market value” (there really is no such thing) of only $100,000 – well, you’d then lose 67% ($200,000 loss on a $300,000 investment) on your “investment” when the speculative period (bubble) finally ends. It only gets (potentially) worse the longer the speculation goes on, and depending on the severity of the “reversion to the mean” when it finally comes…

If we have properly done our job above, we all now understand – in theory – why valuations matter. Unless of course, they no longer do? More on that to follow, which will hopefully now make a lot more sense…

On to the outlook. I mentioned before that we are not going to make the ridiculous “predictions” this year – mainly due to the very wide range of outcomes that all seem equally probable. The following few pages are going to be some of the reasoning behind this – using only a few examples. I promised simplicity.

One thing you will note is that the charts were enlarged this time around. We’ve heard from several people that they tend to read these on their phones, and that the charts prove nearly impossible to see. Hopefully this rectifies that problem – please let us know…

Coming into this year, the vast majority of economists, analysts, etc. were calling for imminent recession – mainly due to the vicious rate increases that had occurred over the previous 12 months, coupled with the inflation that had already occurred. We were less certain on the timing – having noted the traditional lag time between rate hikes and effect on the economy in past cycles – but likely even more cautious than the majority on the ultimate trouble once the lag kicked in. Well, as you may have noticed – no recession materialized. Instead, the economy actually picked up steam. Definitely not on our BINGO card, lag or not.

Now, as always is the case, most all the same prognosticators have changed their tune. The new narrative is “soft landing secured!” Our buddy Jim Cramer only last night spoke about the “beautiful soft landing that Jay Powell has engineered”. Good Lord. He has changed his mind about 27 times this year alone. I digress. Our goal here is to examine data points that might support the current narrative (“all good”) – while at the same time examining others that might support the previous one (“trouble ahead”). The kicker? We’ll be using the exact same criteria to make the case for both. In the end, we think you might reach the same conclusion that we have for the year ahead – in terms of one’s ability to make any sort of credible “prediction” of what is to come.

Important note here. We need to recognize that the stock market is not the economy. For most of economic history, the majority believed that the stock market was a reflection of the economy. This would make sense, as we know that stock prices should be a function of their expected earnings (valuations). So if the economy was weak, we would expect lower earnings, which would lead to lower stock prices….and vice versa. Increasingly, we wonder if the world has become so “financialized” – that the opposite may be true. Said differently, the value of everyone’s stock portfolio (or home) actually led to the strength (or weakness) of the economy – rather than the other way around. Looking at the last two major recessions – or three if you want to count the 3-week “Covid recession” – one could very easily make that case. In fact, Bernanke in no small part justified the advent of quantitative easing – based on this fact alone (wealth effect)…

Either way, it is simply important to note that the stock market and the economy are not one in the same. Definitely correlated (at some point), but not the same. This is the main reason (outside of Fed intervention) that you may sometimes experience an extreme disconnect between markets and your own perception of the economy at large. I’m guessing you’ve felt this disconnect at times over the past several years.

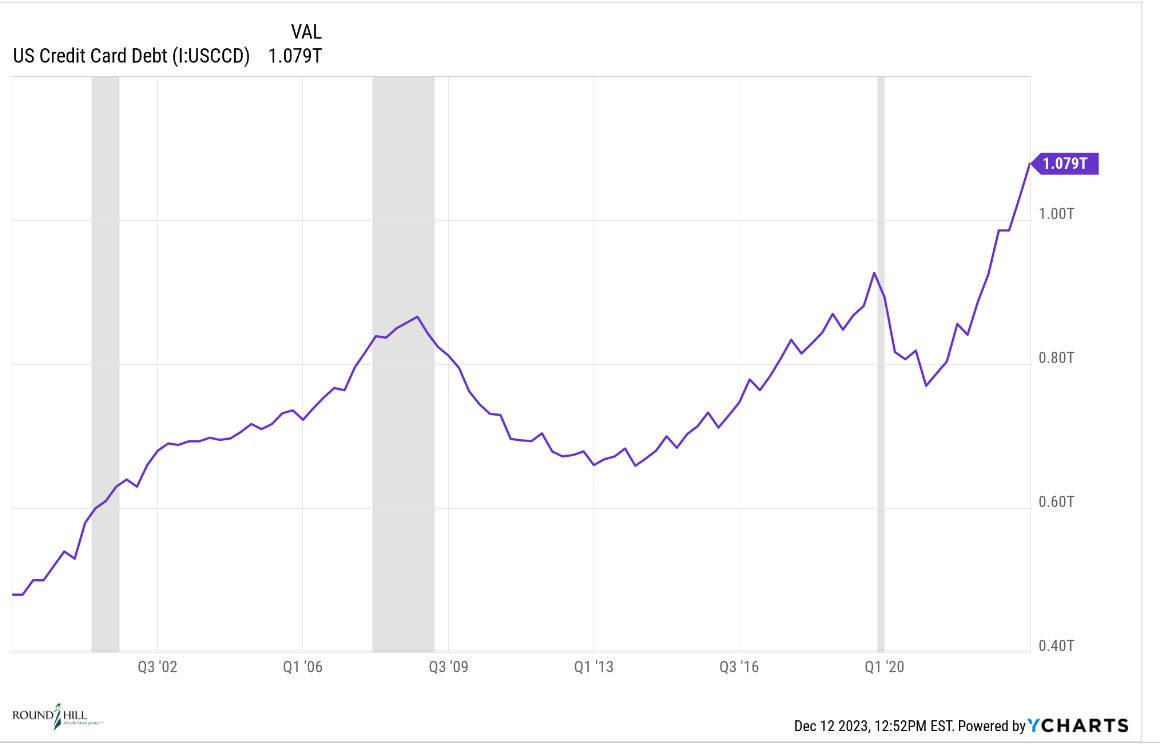

With that in mind, let’s start by analyzing data concerning credit card debt. This has been one of the most analyzed aspects of the economy, as we all try to determine what effect all this inflation - coupled with higher interest rates - are having on the consumer. More simply put, when will the consumer reach their breaking point?

Well, this doesn’t look good – credit card debt at significant, all-time highs. Though it matches what we might expect…

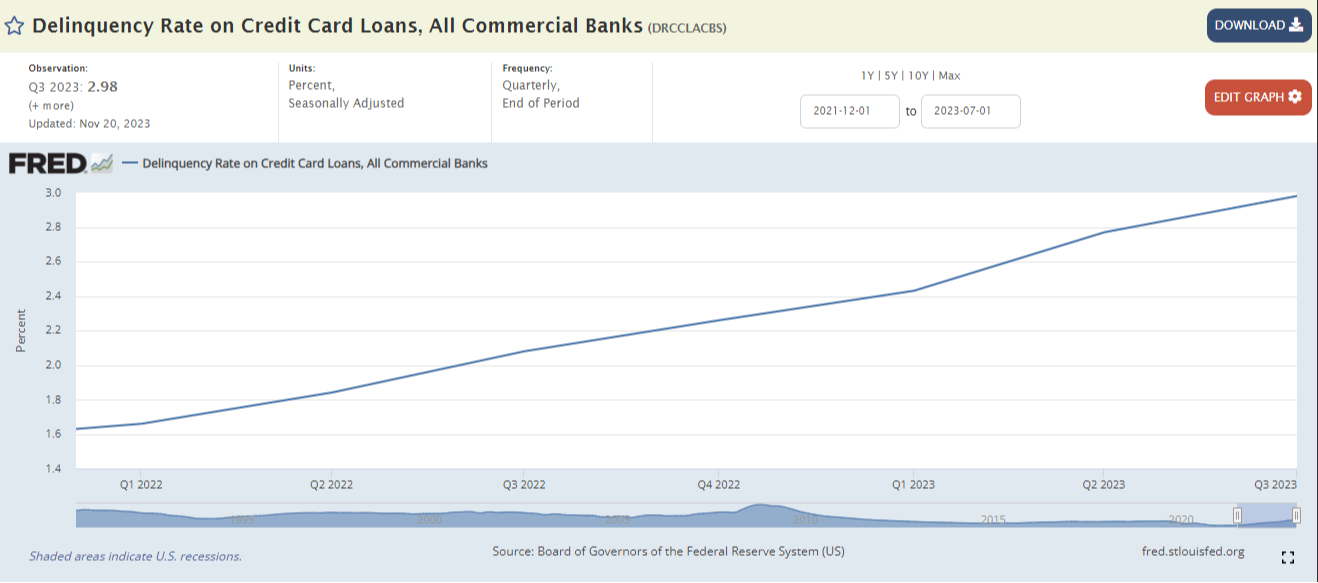

This ain’t good either – delinquency rates on said credit cards screaming higher since this inflation/rate cycle started in late 2021:

So, we can all agree, the situation looks bleak! Credit card debt screaming higher, with delinquency rates on the debt doing the same. Consumer is tapped out. Hard landing (recession) incoming, right?

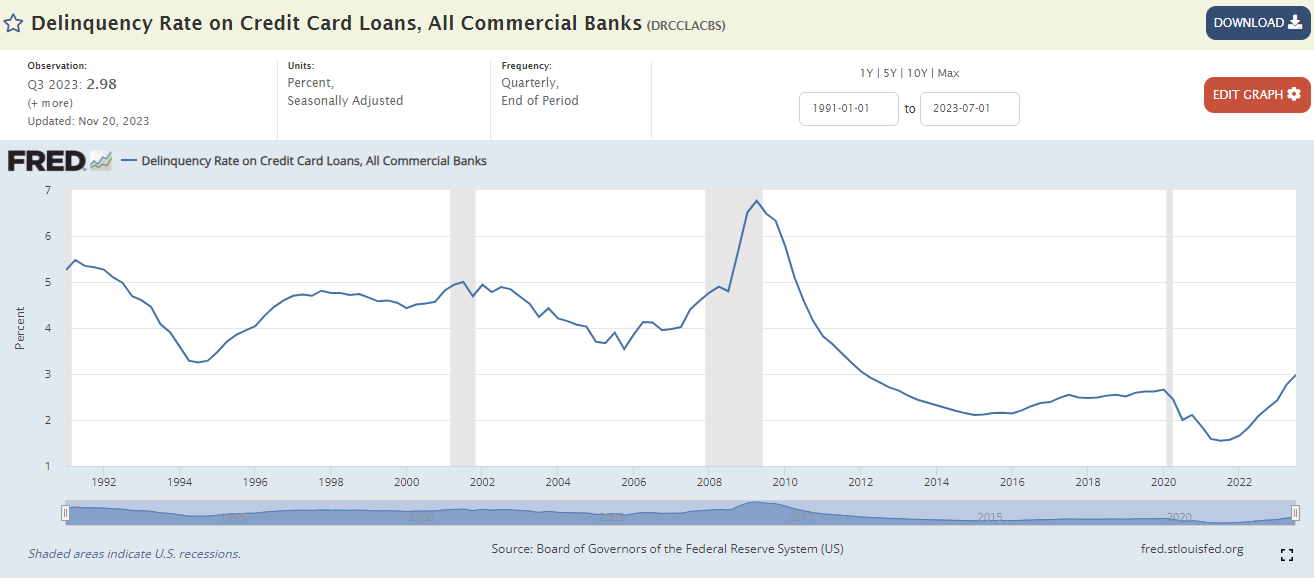

Let’s zoom out a bit for some context:

That doesn’t look nearly as bad! Sure, it’s the highest it’s been in 10 years – and the slope is more than a little troubling – but I’m not sure that we could come to an absolute conclusion on the state of the consumer next year based on studying this data.

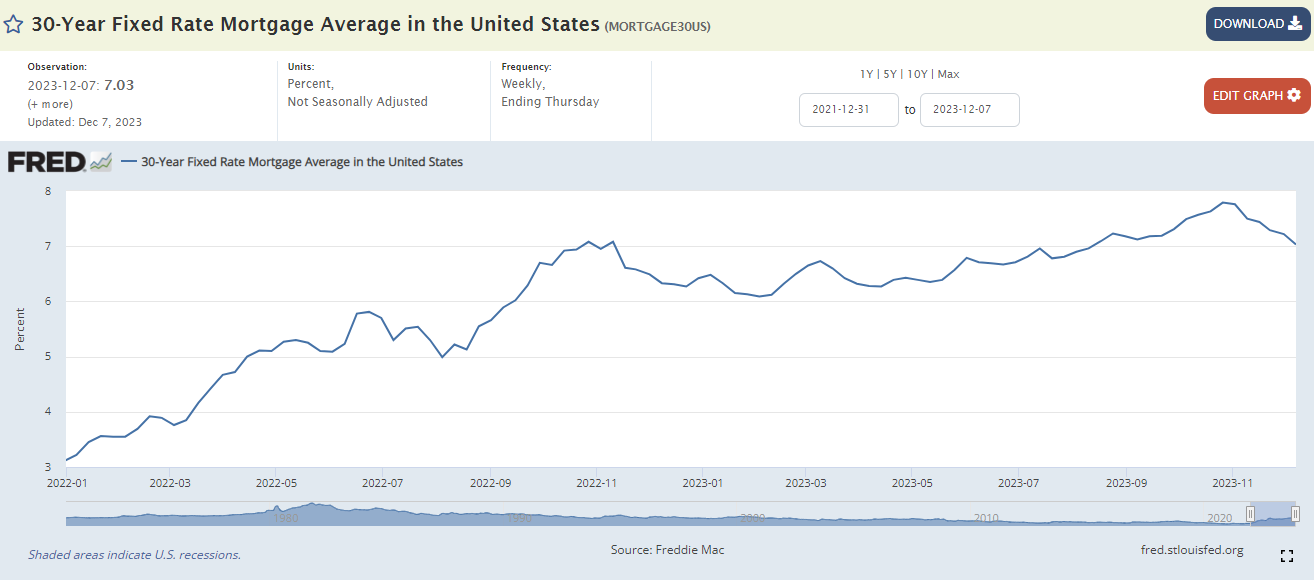

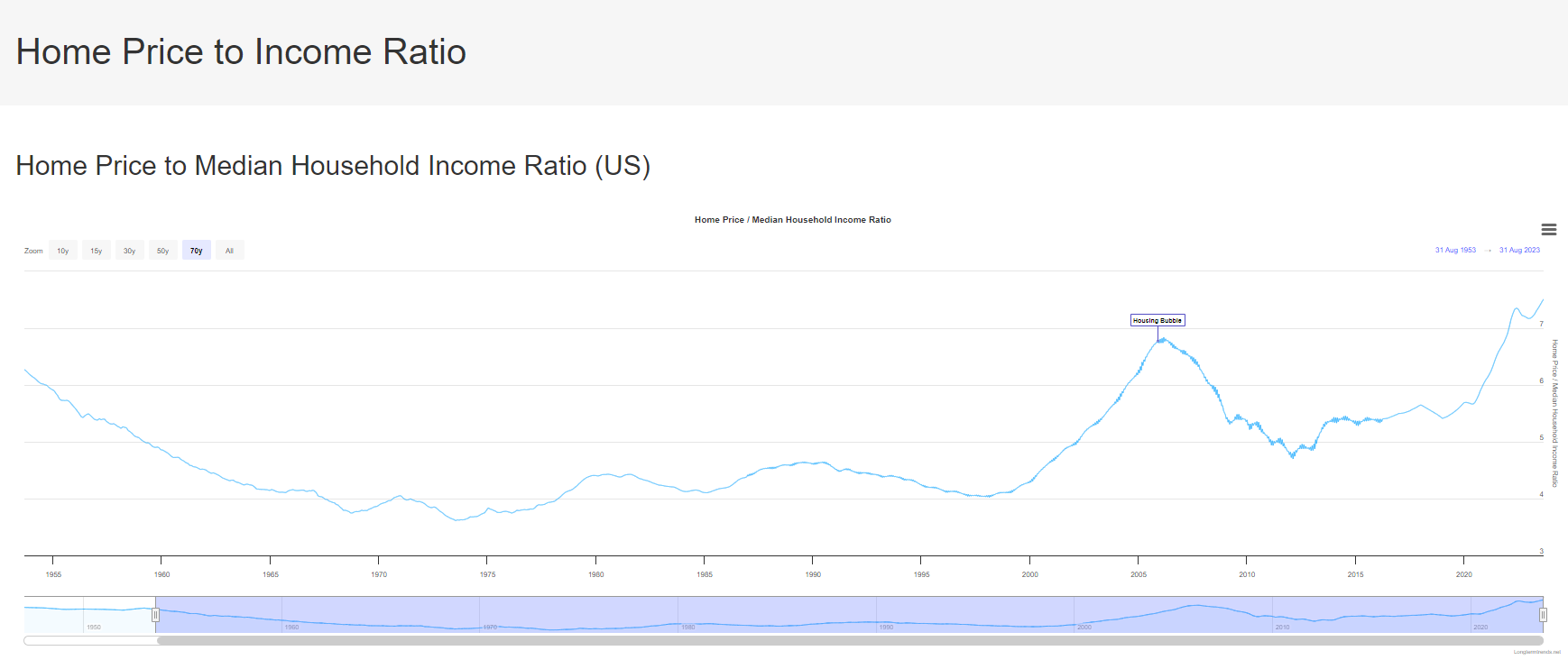

Let’s stick with debt, as it is certainly the most interest rate sensitive aspect of the economy. Now, we will turn our attention to housing. Not home prices – though I have my own theory on that which I will not share here. Instead, we will stay with interest rates as it pertains to housing, and how it might be affecting the consumer next year.

Not new information – mortgage rates have truly exploded higher since this cycle began. Going from near 3% all the way up to near 8% at their recent peak….

OK, I said I wouldn’t get into home prices – but I will anyway. Still not sharing my theory as to how this might end (I’m probably wrong anyway), but rather sharing just so we can see another way the average consumer might be faring. This is a long-term view – and it is the worst ratio in history. Remember, everyone needs a place to live….

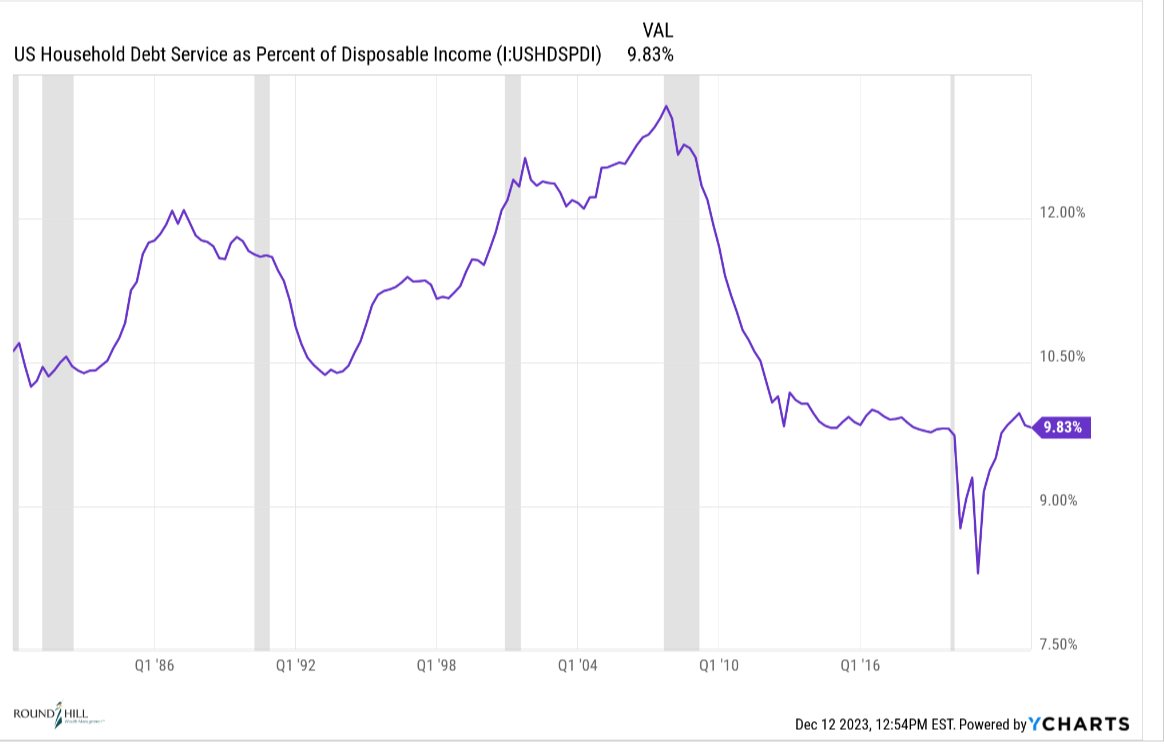

We can all now agree, I think, that the studies above show us that the consumer is definitely pinched by the now much higher rates and much higher prices. Let’s see if we can put it all together, in a historical context, and surmise once and for all that the consumer – and therefore the economy – is toast next year…

Wait, what?? Of the hundreds, probably thousands, of different data sets that we have studied over the course of this year – not a single one was as shocking as the one we just looked at. I was so shocked, I spent an entire evening trying to figure out whether the data was presented wrong, I was interpreting it wrong, or just what the hell I was looking at….

But as we tried to make sense of it, we remembered one thing: ZIRP (zero interest rate policy) for a decade plus. Of course, that’s it. The most obvious example is looking at housing. If you are locked into a mortgage at 3% - and don’t move – interest rates can go to 15% and it doesn’t affect you one bit. Same for your car loan that you took out for 72 months at 0% interest 3 years ago. And on, and on. What this would suggest is that the lag between when rates are hiked and when it hits the overall economy, this time around, may well be longer than in cycles past. This would gel with what we have seen with the consumer – and the overall economy – in 2023. Taking it a step further, one could make the case that – in a bizarre twist of fate - higher interest rates are actually fueling consumers to the extent that their debt obligations remain fixed while the interest they earn on their investments is growing. That said….

Can it be that simple? Our guess is not. What about those who might otherwise be in the market for a new car. Do the now higher prices – and much higher financing costs – cause them to delay as long as possible? Can they afford it? How about those who might want to – but don’t have to – relocate. Are they going to give up their 3% mortgage to buy a home that is now 30-50% more expensive than 3 years prior, and assume a 7%+ mortgage instead? Probably not. Are folks more or less inclined to tap that home equity line at 7% to redo their kitchen? Likely less. Point being, while the most drastic effects of the rate hikes may be yet a few years out, it doesn’t necessarily mean that there is no effect now. Again, very hard to predict over the next 12 months.

Circling all the way back to where we started – “data” vs “experience”. The data is impossibly conflicting – especially in the very short-term (the year ahead) – while our “experience” tells us that the combination of the most significant inflation in some 40 years coupled with interest rates going from 0 to 5%+ at the fastest clip in history will not likely pass without consequence. You now know why we are not making “predictions” for the year ahead – we’d be better off and much more entertained bringing in a monkey (no offense to monkeys) to offer an intelligent prediction on the economy next year. But the analyses above also help explain why we are much more comfortable analyzing economic conditions over a 1-3 year time frame, rather than simply 2024. Based both on “data” and “feel”, we would suspect trouble ahead – subject of course to countless developments that could reveal themselves over the coming year (most having to do with interest rates and the Fed).

Let’s now wrap this up by moving away from the “macro” (boogie, woogie, woogie), and focusing specifically on the markets and your money – especially since we all now know just what we are talking about with these “valuations”…

Not going into interest rates and bonds, other than to say the following:

Tell us how the macro environment as analyzed above plays out in the coming year – a task which we have hopefully made clear is near impossible – and we will tell you whether you would likely be better in bills (short-term) or duration (longer-term). Only a month ago, we were leaning (and positioning) toward the latter. With rates now having dropped parabolically in only a month – without a clear economic reason for doing so – it is much less clear heading into next year. Our plan is stay more “balanced” for the time being, and react as the situation develops. To be clear, however, our preference would be to add to duration if the opportunity (higher rates) again presents itself – or if the economy begins showing signs of significant deterioration ahead. The problem with the latter is that the bond market would likely beat us to the punch.

OK, I lied – one more note on the income space while we are at it. As we have talked about with many of you already, it is not as easy as it might seem to weigh short-term (T-Bills, or money markets) against duration (longer-term maturities). While it may seem simple to say, “If I can get over 5% interest – without any market or interest rate risk – why wouldn’t I have all of my money there?” First answer is this: It’s tempting, especially considering the environment described above. But what if the economy falls off a cliff – and short-term interest rates return to where they once came as a result (zero)? Now, you are left with a pile of cash again earning next to nothing – and worse yet – you achieved no principal appreciation as the rates fell…

Conversely, if you were to buy a 10-year government bond instead, either of the following would be true. First, if you chose to hold the bond, you have now locked in your (currently) 4% interest for the next 10 years. Second, if you chose not to hold your 10-year bond to maturity – say because valuations on stocks became much more attractive in the process – the value of your 10-year bond is going to have appreciated considerably. Of course, the opposite is true if rates were to increase significantly instead.

That’s enough to be dangerous, and the decisions as described above remain at the top of our focus list – while the next topic remains at the top of our “frustration list”….

We will begin with - since all of you are now officially experts on the concept of valuations - another chart for your perusal, followed by a discussion of what it might (or might not) mean…

As stated on the chart, this is showing the Shiller PE ratio over the entire history of the S&P 500. Let’s revisit what the Shiller PE is, but using our hypothetical from earlier. Basically, a “PE Ratio” is measuring how cheap or expensive a business might be, based on it’s current earnings as a percentage if it’s price. Using our example, if the cost to purchase our business was $100,000, and it produced an average of $6,000 of earnings per year over the past 10 – it would have a “Shiller PE” of 16.7 ($100,000 divided by $6,000). The real Shiller PE does the same, except it factors in the past 10 years worth of earnings – and adjusts them for inflation. Remember, any business has some degree of cyclicality – as well many other risk factors overall. The Shiller PE attempts to adjust for that uncertainty by using a longer time frame. The higher the number, the more expensive the stock (or business) would be considered.

Currently, the Shiller PE on the S&P 500 index is around 32 (I’m a week into writing, and stocks only go up apparently). Using our hypothetical, that would mean we would have to pay about $192,000 for our business that was averaging $6,000 of annual profit. Our “earnings yield” using those parameters would be about 3.1% - compared (today) with government T-bills paying over 5% interest, and 10-year government bonds paying near 4%.

What I have highlighted in the chart above is what we call our “100 trillion dollar question”. It is the question that keeps us up at night. It is the question – whether they admit it or not – that every single money manager in the world is trying to answer, even if they choose to ignore it. The question is this:

“Why, for over 100 years, have valuations on stocks largely remained in a particular range – but for the past 30 years or so – (largely) been in an entirely different (higher) range?” Asked differently, the question would be “Should we ignore 100 years of stock market valuations - in favor of the past 30 - and if so, why?”

Our attempt at answering that question is another 20 pages at least – not happening here. Successfully answering it would allow one a remarkable advantage in managing both risk and return in portfolios. But while we each and everyday work toward answering it, I will give you our answer so far:

“We don’t think so, but remain open-minded.”

The obvious way one would attempt to answer the question would be to start with, “What has changed in the past 30 years?” In lieu of the aforementioned 20 pages, here is a list of what we consider most closely, in no particular order of importance:

- Interest Rates

- Accounting Rules (how earnings are measured)

- Stock Buy Back programs

- Passive (index) flows and 401k accounts

- Fed / Government Intervention

Again, would truly enjoy input from those reading along on the question above, and it leads us into the final section of our outlook…

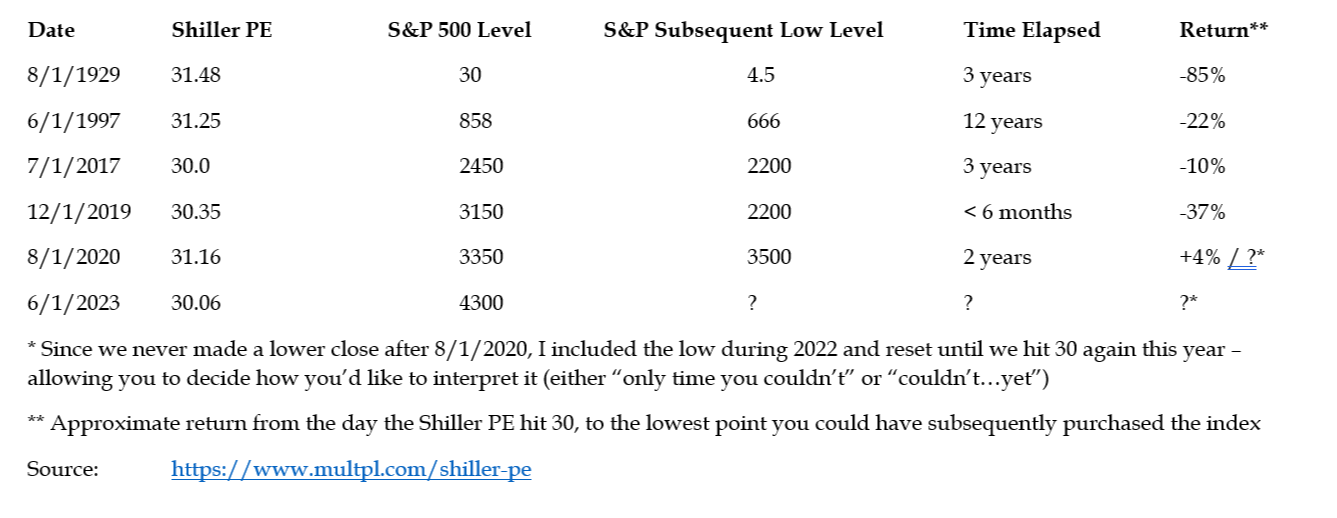

We are concluding with one last “which is the more important data” analysis as we head into the new year. Below are the results of a study that we did earlier this year – as we were again approaching 30 on the Shiller PE. We wanted to answer the question, “How many times were there in history, where the Shiller PE reached 30 – and you couldn’t buy the S&P 500 at a cheaper level at some point in the future?” I know, that’s a mouthful. We did not know the results ahead of time – though we suspected that the answer was “not many”. We were surprised, but not in the way we thought….

The results below are using “round numbers” (I was going to drill it “down to the penny”, but quite honestly, I’m out of both time and energy at this point) – you can visit the source listed below if you’d like to confirm the numbers yourself (it is a GREAT source of info by the way). I went through every month through history, to find the times where we hit 30. Once it did – and if the market subsequently traded at a lower level at some point in the future (in other words, you could have waited it out and bought cheaper) – I then waited for it to again hit 30, and repeated the process. Here are the results (again, all numbers approximate) and the important details:

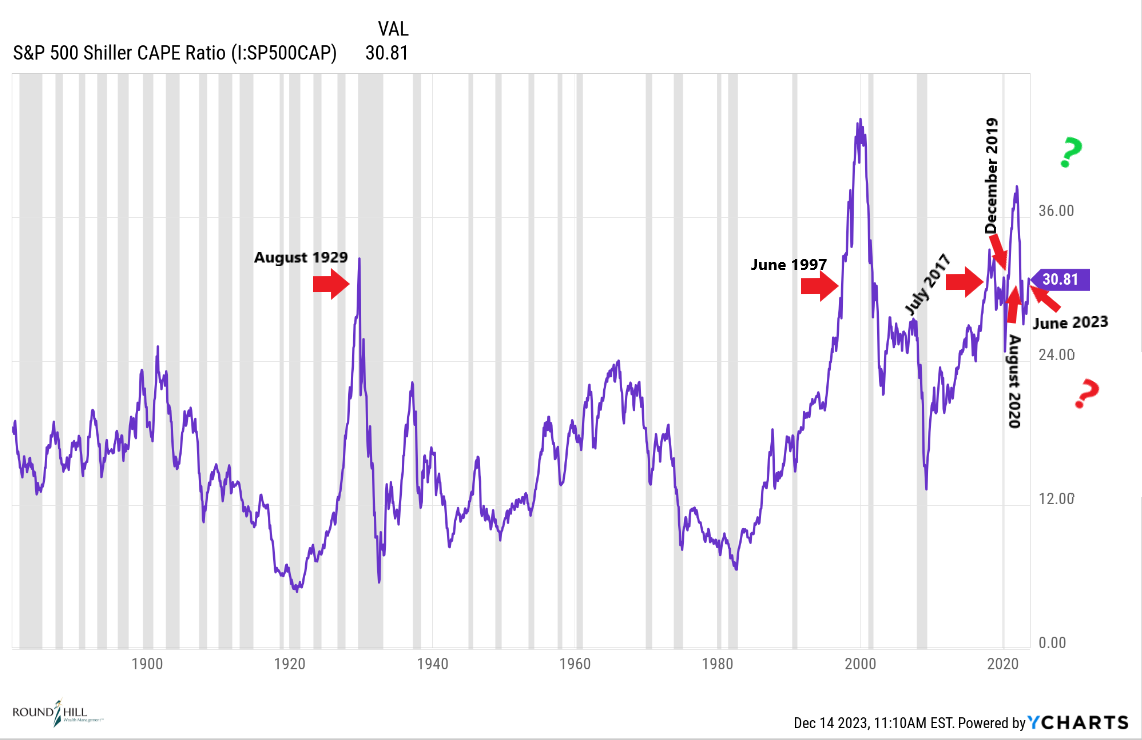

Below is a chart showing each of these occurences on a long-term chart of the Shiller PE for the S&P 500 throughout history. Ask yourself what stands out most as you review it…

What stood out to us you might ask? Two things. First, the concentration of these instances just recently. Second, the magnitude of the “reversions” previously. This time different? Wish we knew. The “10 trillion-dollar question”….

But before we all start assuming that stocks are doomed for the year ahead, let’s consider one last piece of information:

“The good news for investors heading into 2024 is that the S&P 500 has not declined during a presidential re-election year since 1952 and has averaged a 12.2% annual gain in re-election years.”

Source: https://money.usnews.com/investing/articles/election-2024-how-stocks-perform-in-election-years

Oh we know they are gonna try and pump it baby! Our President just released a video on Twitter, touting “his” recent stock market performance. Interesting timing, right after the J-Pow shocker. Things that make you go hmmmmm….? Yellen has already started (as mentioned previously) – and I’m sure there’s a few billion here or there from Covid/ “The Inflation Reduction Act” that can make its way into the system. Every administration from every party plays the game – and like everything else of late, they just don’t try to hide it as much anymore. But at this point, you don’t need us to remind you, that allocating to stocks on the basis of any of this is the very definition of “speculating over investing”. Doesn’t mean it won’t work, it very well might again in 2024. But based on all that we have discussed today, we need to be honest enough to call it what it is...

In conclusion, we want to reiterate one last time just how wide the range of outcomes truly is for the year ahead – in our view - for the economy, asset prices and certainly the entire geopolitical landscape. We hope we have at least somewhat adequately laid out our case for this belief within the pages of this update. Still, we hope that we have also adequately laid out our case for both the challenges and opportunities that we might expect, using a slightly longer timeframe. While it is hard for us to make a credible case for the long-term risk/reward profile of stocks being a favorable one – with valuations on the largest indices (specifically) as discussed – it does not mean all is bleak. In many ways, we would argue the opposite…

For one, there is now an extreme diversion between the “Magnificent Seven” – or the S&P 500 as a whole because of it’s concentration in such – and “the rest of the market”. Because of this diversion – and the pain that has been felt under the surface over the past two years – the “rest of the market” is not nearly as expensive as the S&P 500. We wouldn’t necessarily call it “cheap”, but it certainly is on a relative basis. Let me preface the next statement with the following: This is not 1999. It’s not 2008. It’s not 1974. And it is not 1929. The year is, in fact, 2023. With that out of the way, we can make a comparison of sorts to the late 90’s. In that period, much like today, “growth” (specifically anything to do with this new thing called “the internet”) was all the rage. It was during this period that the Shiller PE on the S&P 500 reached it’s historical peak. Much like today’s “Magnificent 7”, technology became more and more concentrated in its weighting of the index.

Meanwhile, “value stocks” couldn’t catch a bid. Ultimately, when the “bubble burst”, the S&P 500 lost over 50% of its value from peak to trough. Many “value stocks”, on the other hand, not only didn’t participate in this downtrend – they actually went up. To be fair, value stocks were much “cheaper” back then than they are today. And if I didn’t make this clear above, the year is not 1999 – past performance is never a guarantee of future return. The point being that not all stocks today are subject to the extreme valuations we have discussed. Or, using our hypothetical, there are still companies that “we can buy with our $100,000”. But for the vast majority of this year, these “value stocks” have not participated in any meaningful way with the vicious rally in the S&P 500 – which as I noted previously, was the biggest source of frustration for us. We view the reversal of this trend, should it occur, as a potential opportunity in the year ahead. But not as important as the opportunity we will discuss next…

For the vast majority of Round Hill’s existence (now 10 years), interest rates had remained at or near zero. That all changed beginning about 18 months ago, and it is a huge benefit to all investors – but particularly those investors at or near retirement, or with a lower threshold for risk. Though we spent the majority of this update discussing the economy and stocks, this change in the interest rate environment should not be ignored. With a balanced and tactical approach, we now have the ability to lock-in interest rates where warranted – with significant principal appreciation to boot, should rates ultimately decide to reverse lower. Additionally, investors have at their disposal short-term rates (T-bills currently paying over 5% interest) – offering both a higher interest rate and protection against rates deciding to continue higher. Again, much more could be said on this topic, but the importance of this development could not be overstated for most of you reading this.

A final note. Some of what I am about to say we have shared many times before in these updates, but oblige us if you would. Every single one of you reading this has different goals, timeframes, experience and tolerance for risk. But I will always submit that every investor in the world shares one common “golden goal”: never outliving one’s money. We spend all of our time discussing and analyzing what we have shared with you today, on top of the additional 200 pages which would be required to cover the rest. But all of it, always, is toward executing a strategy on your behalf - with that “golden goal” in mind. Long-term, not short. We cannot control markets or interest rates, and there is no what “should be” in the world of investing one’s money. We play the hand we are dealt, as best we can.

To make matters more complicated, “emotion” is an evil little bugger when it comes to investing. One of your wealth advisor’s primary job functions is to help take emotion out of the decision-making process. I would argue it may be the most important. It is most commonly referred to during periods of market turmoil – helping clients stay invested so they don’t “sell the bottom”. Dealing with fear.

But we rarely hear about the other side of the emotional coin – that being “greed”. Equally powerful, in fact most studies suggest that it is a bigger emotional driver for investors than fear. Would make sense, given the countless speculative bubbles over time (tulip mania being the most fascinating by far). As the kids would say, dealing with FOMO (fear of missing out).

I’ll let everyone in on a dirty little secret. I think some assume that since it is our job to remove emotion from investment decisions (it is), it means that we as advisors don’t feel said emotion ourselves. That, emphatically, is false. We are always acutely aware of the investment environment around us, obviously, as it is our job – and how it might affect the psyche of our clients. We are not immune to your feelings. But if we are doing it right, it is our job to “eat the emotion (panic)” during periods of turmoil - and also “eat the emotion (FOMO)” during periods of euphoria – on behalf of clients, so as to maintain a clear-minded and long-term focus. The “eating” of said emotion is a stressful exercise, and the longer it goes, the more stressful it becomes. I can speak for Dave in saying, our bellies are now more than full. To the extent you might wonder how we can almost robotically share some of the information we do, particularly around “valuations” – even when what you see on TV might seem to suggest otherwise – the answer is somewhat frustratingly simple:

We are removing the emotion.

That in no way should imply blind rigidity, or an unwillingness to adapt – the landscape is always changing, and it is also our job to recognize and try to make sense of these changes as they occur. Our goal in these updates is to communicate our efforts toward this end. But data is not emotional. Math is not emotional. History is not emotional – though our perception/interpretations of it may be. This is where experience comes into play, as historical data is much more “useful” when you’ve actually experienced it, for the much-needed context. “Book smarts” and “street smarts”. Both important, but neither offer guarantees of what is to come – especially true in any short-term period.

The one guarantee we can give you is this:

In terms of any and all that we have discussed today, there simply is no such thing as “common sense”….

With that, we thank you for reading, and want to wish you and your families all the very best for the holidays and for the year ahead! And to all of our clients, as always, we can never thank you enough for the continued trust and confidence you have placed in us.

The opinions expressed in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

Statements of forecast are for informational purposes and are not guaranteed to occur. Trends discussed are not guaranteed to continue in the future.

All performance referenced is historical and is no guarantee of future results. Investments mentioned may not be suitable for all investors.

Equity investing involves risk, including loss of principal. No strategy – including tactical allocation strategies - assures success or protects against loss.

Value investments can perform differently from the market as a whole. They can remain undervalued by the market for long periods of time. There is no guarantee that any investment will return to former valuation levels.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index is a capitalization weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major indices.

The NASDAQ Composite Index measures all NASDAQ domestic and non-US based common stocks listed on the NASDAQ Stock Market. The market value, the last sales price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the index. You cannot invest directly into an index.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

The prices of small-cap stocks are generally more volatile than large-cap stocks.

The fast price swings in commodities will result in significant volatility in investor’s holdings. Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Any discussion regarding gold or commodities in general is referring solely to the asset class(s) themselves – we do not directly hold physical commodities or gold.

Securities offered through LPL Financial. Member FINRA/SIPC. Investment advice offered through HighPoint Advisor Group, LLC, a registered investment advisor. HighPoint Advisor Group, LLC and Round Hill Wealth Management are separate entities from LPL Financial.